[vc_row][vc_column][vc_column_text]

A helpful blog by moneyweb to put our clients at ease.

Read the original here.[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][vc_column_text]

Investing

Covid-19 market crash: Lessons for investors

The Covid-19 global pandemic has caused ripples through global financial markets as the virus continues to spread across the globe and governments battle to find the right measures to contain it.

We still do not know what the eventual impact will be, and how the pandemic will impact countries, markets and families. From a financial and investment perspective, we can stand back from the current crisis and reflect on the anatomy of a crash and how markets behave during and subsequent to a crash.

We should expect a market crash every six years.

A market crash or bear market is defined as a market correction where the market falls by more than 20% from its previous high. Looking at the biggest stock market in the world, the US, the S&P 500 (the broad measure of the US market) has experienced 16 bear markets since 1926, averaging one bear market or correction every six years. The average of these market losses has been an eye opening 39%!

From the above, it is clear that South Africa is part of the global village and we are exposed to global market shocks. Except for the Soweto riots, it has taken between 18 and 30 months for the market to recover back to their previous highs following a shock.

Lesson 1. Markets have historically recovered from a crash

Markets are erratic

It is impossible to predict market returns, specifically during a crash when markets are reacting emotionally and erratically. This is clear in looking at share prices during the last week and by merely looking at the headline of one share, Sasol.

• March 12: Sasol loses another 40% of its value in an hour

• March 13: Sasol surges 45% after announcing sale of stocks and assets

The above is an example of how erratic the market can behave during a stock market crash, thus in a few days you could have lost 40% or made 45%.

If we stand back from a specific share, and look at the market as a whole, the US sub prime crisis (also know as the financial crisis) resulted in the JSE correcting by 42%. In 2008 alone, the South African market fell by just over 30%. Even though it was impossible at the time to determine when the market would recover, the crash of 2007/2008 was followed by exceptional returns in 2009 with the market recovering by more than 20%, followed by double digit returns in; 2010, 2012 and 2013. Investors where thus rewarded for staying the course, as per their financial plan and objectives.

The extreme volatility is also evident in returns the last week, amidst the Covid-19 pandemic:

• March 11:US (S&P) selloff approaches 20%, what next?

• March 13: US market scores biggest gain since 2008, S&P 500 jumps by 9.28%

This short-term uncertainty can create destructive behaviour as investors react emotionally and disinvest amidst the market noise and uncertainty.

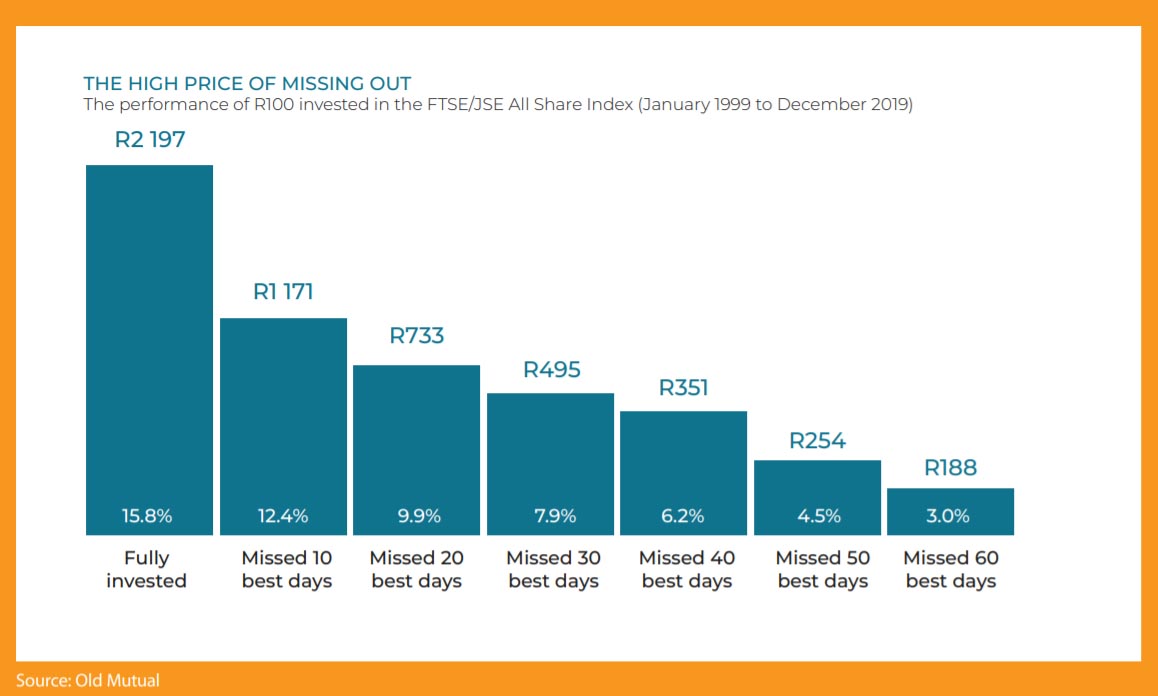

It is important to remember that in disinvesting from the market, there are two decisions to get right; the right time to disinvest and the right time to reinvest in the market. Thus, investors must get both the exit and entry prices correct which is extremely difficult.

The probability of timing the markets is summarised in a research study conducted by Vanguard (one of the world’s largest asset managers):

“The biggest takeaway from our analysis is that the probability of being lucky and outperforming the benchmark is already less than 50% when taking just a few days out of the market. This probability then decays rapidly as the number of days out of the market increases. Unless an investor has great skill and/or luck and the conviction to act on these insights, the most effective approach is to remain invested.”

The risks in attempting to time the market are further illustrated by the research conducted by Old Mutual Investment Group.

Lesson 2. Markets can be crazy during a crash and are impossible to time. Stay invested.

Your portfolio should reflect your financial personality.

It is often said that diversification is the only free lunch in investments. The principle behind diversification is investing in several different asset classes or investment types i.e. South African: equities, fixed interest and property and international: equities, fixed interest and property.

The spread of investment risk (diversification), reduces the exposure to any one asset class significantly underperforming.

Diversifying into international assets acts as a handbrake during global market uncertainty or market corrections. As investors withdraw from emerging markets (which are perceived as risky) and invest into developed market bonds (which are a safe haven in times of uncertainty) emerging market currencies depreciate. In such a scenario the offshore exposure in an investor’s portfolio benefits from rand depreciation, even though the underlying asset prices may be falling.

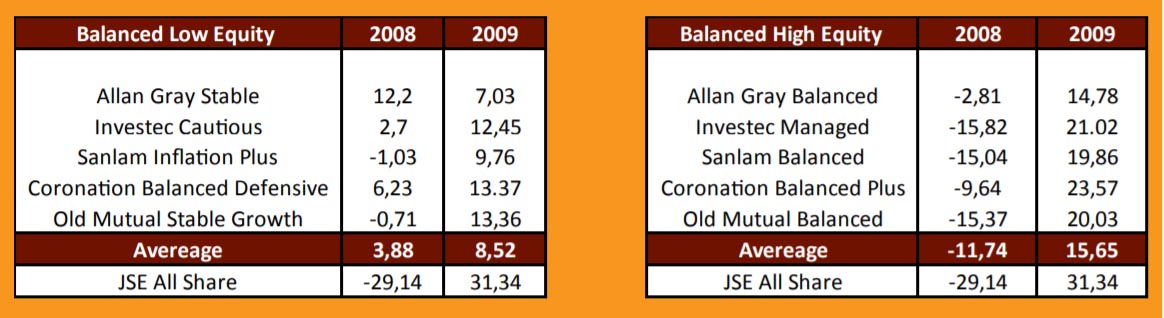

The below illustrates the benefits of diversification by investing in a balanced portfolio during the financial crisis in 2008:

Balanced low equity funds represent a portfolio for conservative investors where the equity exposure is limited to 40%, the equity exposure can go up to 75% in the balanced high equity funds, which is more suited for moderate or growth investors. In both the aforementioned funds, the offshore equity exposure may be up to 30%.

The above analysis illustrates a few important investment principles, that will apply in most market corrections or crashes:

• Markets recover after sharp losses or bear markets

• Balanced funds provide investors with protection against market corrections.

• Balanced low equity funds provide significant protection during periods of uncertainty. They do however significantly lag during the “recovery phase”.

Investors often switch to low equity balanced funds during times of uncertainty, this can result in them missing the market recovery and only switching back to higher risk balanced funds subsequent to the market recovery. Timing is a mugs game, investors need to stay true to their specific risk profile and appetite; through both bull and bear markets.

Lesson 3. Diversification is the only free lunch and protects investors during a crash

Your money personality (risk profile) should not change during a crash.

Guaranteed annuities (pensions) provide a sense of comfort during bear markets.

During recent years we have seen an increase in the interest in traditional or guaranteed life annuities. Guaranteed life annuities are provided by insurance companies including Old Mutual, Sanlam, Discovery, Liberty and Just SA who guarantee an income for life. There is a wide variety of guaranteed annuities, with the most popular being inflation linked and with profit annuities.

Investors’ pensions payments are protected through very strict governances and regulation requiring that insurers hold sufficient capital to back their liabilities i.e. pensions owed to investors. These capital adequacy ratios require that insurers hold enough capital to make provision for market shocks or corrections.

Thus a “normal” market correction should have very little impact on insurers’ ability to continue paying pensions. Investors invested in life annuities that provide inflation-linked increases have little reason for concern as their future increases remain linked to inflation. The annual increase of with-profit annuities is linked to the performance of the markets and, depending on the insurer, is linked to market returns over i.e. a five to six-year period.

It remains difficult to determine the impact of the current market turmoil on investors invested in with-profit annuities. Should the turmoil continue, and markets not recover, they may be faced with zero increases.

For many retirees, with-profit annuities provide an effective annuity or pension strategy, if used appropriately with other annuities or the provision of an emergency fund. The benefit of with-profit annuities is higher pension over time.

Globally the flight to safety has had a negative impact on retirees wanting to invest into life annuities. Annuity rates largely depend on bond yields. Global bond yields (which were already low) have fallen even lower as investors pile into bonds which are perceived as a safe haven investment. This has resulted in a decrease in annuity/pensions for retirees in many developed markets.

We have not yet seen the same impact in South Africa, with long bond yields remaining relatively stable, thus the SA life annuity yields (starting pension) have remained relatively stable during the last two months.

Lesson 4. Traditional life annuities or hybrid annuities provide some comfort during a market crash

What should investors do?

It is almost impossible to predict how the markets will react or recover during this pandemic. The following are a few principles that investors can follow during this time:

Stick to your plan

Your financial plan should be developed to consider your personal objectives and your risk profile. It is important to review your plan to ensure this still aligns to your objectives. However, be wary of changing your “money personality” due to the noise and the crisis, your risk profile should remain intact during both bull and bear markets.

Let the professional money managers do their job

A diversified investment portfolio should include several investment managers and investment mandates aligned to your risk profile. The investment managers will align the underlying portfolio to the current market conditions and increase or decrease the equity exposure within the parameters of the mandates to mange your portfolio and risk on your behalf.

Now is the time to be frugal

If you have not made provision for an emergency fund, now is the time to be cautious, save on luxuries and where possible build up a buffer or emergency fund. Given the continued uncertainty it is important to diligently manage expenses and increase the allocation to your emergency fund. It is now more prudent to be conservative with your finances than to overextend during these times of uncertainty.

The Covid-19 market crash is a shock, and we are all concerned about how this virus will be contained. From a financial perspective, it is important to remind ourselves that this is not the first crash we have seen, and certainly won’t be the last crash that most investors will experience.

A well-structured financial plan, implemented through a diversified portfolio, will assist in delivering on investors long-term objectives through difficult markets.

Wynand Gouws is a certified financial planner at Gradidge-Mahura Investments.

The views and opinions shared in this article belong to their author, cannot be construed as financial advice, and do not necessarily mirror the views and opinions of Moneyweb.

[/vc_column_text][/vc_column][/vc_row]